We are delighted that our Martin Currie Australia (MCA) Sustainable Equity strategy reached its three-year anniversary in May 2023 with positive gross and net of fee alpha1. We also excited for what the current market environment can bring for future performance

In this article, we delve into the five key factors and considerations that have underpinned the sustainability and financial credentials of MCA Sustainable Equity portfolios since launch. These include strong in-house sustainability and financial research, a consideration of carbon transition risk, a limited lack of negative exclusions, the use of active ownership, and a distinct value-style to investing.

1. An in-house team uncovering strong Sustainability attributes

The Sustainable Equity strategy was designed for investors who increasingly want to generate healthier outcomes for stakeholders without forfeiting the financial returns from their investments.

Our approach is premised on the belief that companies should be more successful financially and have longevity if they are also sustainable. Our team of research analysts and portfolio managers specifically seek companies that we believe can provide Net Sustainability Benefits to society, have a board and management team that focuses on their Sustainability Risks and opportunities, and have a clearly articulated Sustainability Pathway towards a more sustainable environmental, social & economic future.

We are very strong believers that Active Ownership – i.e., ESG analysis, engagement, and voting – should be done directly by those making investment decisions rather than being outsourced. To us, investors are best positioned to develop an informed view of the ESG risks, opportunities and impacts that companies face or create. Therefore, at MCA this responsibility lies directly with our experienced team of research analysts and portfolio managers.

The development of the Sustainable Equity strategy was a natural extension of MCA’s investment philosophy. Sustainability inputs and assessments have been embedded directly into our investment process since 2009, the year we became signatories to the PRI.

MCA’s ratings framework: a common language for Sustainability analysis

analysis

| Sustainability Risk | Common Sustainability risk factors faced by a company and its industry, as well as their materiality |

| Net Sustainability Benefit | A company’s overall impact on society |

| Sustainability Pathway | Change in the ESG factors that are likely to improve for a company when analysing the company's operations, products and services. |

We are very strong believers that Active Ownership – i.e., ESG analysis, engagement, and voting – should be done directly by those making investment decisions rather than being outsourced.

2. Quantified carbon transition risk

We have developed a proprietary Carbon Value at Risk (VaR) tool to assess the sensitivity of each stock and the portfolio to climate transition risk. Our tool looks at how a company’s valuation could be impacted by applying a “Shadow Carbon Cost”, and this helps us to identify stocks that will either benefit or have a minimal impact on their earnings from the energy transition.

Importantly, our analysis takes Scope 1, 2 and 3 carbon emissions into consideration. Scope 1 and 2 emissions can be mitigated by investment in new technologies to replace and reduce existing assets that contain high carbon emissions, but it is Scope 3 emissions, which we believe better reflect a company’s strategic risk with regards to carbon.

3. A financial grounding and high quality stocks

As with all MCA strategies, the Sustainable Equity investment process starts with bottom-up fundamental research by our specialised industry analysts. The importance we place on proprietary research into long-term normalised earnings power, cashflow sustainability, business quality and risk, is reflected in the size, quality, and experience of our investment team.

Our analysts’ independent insights on the risks and opportunities across the investment universe are captured in a consistent manner via MCA’s proprietary research lenses - Valuation, Quality, and Direction. By incorporating material and relevant ESG factors into our Valuation and Quality lenses, our investment process specifically reflects how ESG factors can increase or reduce the risk of companies delivering our forecasted expected returns.

MCA’s proprietary research lenses capture ESG factors

| Direction | We consider the direction of earnings changes, and short- & long-term earnings factors. |

| Valuation | We include any impact of material and relevant ESG factors in our normalised earnings and fair value estimates. |

| Quality | We include our Management, Governance, and Sustainability |

Our Sustainable Equity strategy process facilitates tilting of the portfolio towards companies with good sustainability characteristics and low shadow carbon costs while maximising expected returns. Stocks with poor sustainability issues such as high carbon footprints, unsustainable business practice, stranded assets, or poor future sustainability outcomes, are penalised through this portfolio construction process.

4. Harnessing the power of active ownership

We have developed strong ongoing relationships with investee companies but are not averse to challenging them about their progress to a more sustainable pathway. By doing this we can encourage greater transparency, ask more insightful questions, gain greater insight into the company’s management of key ESG issues, and ultimately, nudge companies towards real change, more sustainable business practices and long-term value for our clients.

To us, Active Ownership is an integral part of being an investor and a long-term owner. We recognise that engagement is an iterative process which requires patience and persistence. Our investment team’s long-term experience with management engagements bolsters our ability to effectively affect company level changes. We have cultivated strong relationships and established open dialogues giving us the opportunity to express any areas of concern and encourage greater transparency on their management of these risks.

5. Focus on active pathways, rather than exclusions

Traditional sustainability funds are often highly focused on tech stocks as they have low/no carbon emissions. On the other hand, they shun energy companies, manufacturers, and utilities, which are typically seen as Value-style stocks. Many of these funds may have what looks like good sustainability scores due to low carbon emissions, but the questions for us are, “what are they doing to contribute to a more Sustainable future, and are they overvalued based on this low future contribution?”

The push for companies and countries to adopt Net Zero targets is driving substantial investments in energy transition infrastructure. There is a significant opportunity for Australia to help the rest of the world to decarbonise, owing to our notable solar capacity, and large presence of resources and service providers (often classified in the energy and utilities sectors that sustainability funds exclude). Australian companies stand to benefit from the pipeline of work, now and over the coming decades.

We want to point out that we have intentionally created a strategy that focuses on a company’s overall Sustainability Pathway, rather than employing a range of negative screens. This distinguishes our approach from many ESG funds where negative screening is the primary focus, and also means we are more Value-style titled than most peers. We have however purposefully screened out activities such as the production of "controversial weapons " and the manufacture of tobacco products as we see no sustainable pathway available for these industries.

A stock’s carbon emissions today also doesn't take into consideration any work being undertaken to improve. Our proprietary Carbon VaR tool helps us to avoid those stocks that are unlikely to survive in a low carbon future and the focus on those that may be high emitters today but are making the transition.

To facilitate real change, we believe that it’s important to have a seat at the table as investors and proxy voters. Excluding companies based on specified activities removes an opportunity to work with companies to move them towards more sustainable practices, and benefit financially from that shift as companies move forward. Avoiding certain sectors can also leave investors exposed to style risk, which we saw during 2022 when Value came back into favour relative to Growth.

The current inflationary conditions continue to provide a tailwind for the Value style, including those with stronger Sustainability attributes, while Growth stocks are expensive and Value stocks are still far cheaper today relative to history. As these extremes will inevitably unwind, we see that the Valuation starting point for excess returns to Value investing remains strong for the next decade.

The end product: a portfolio with Sustainability and financial credentials

Our dedicated focus has resulted in a Sustainable Equity strategy that we believe is well positioned with both attractive sustainability and financial attributes. Relative to the S&P/ASX 200, the portfolio has2:

- Better MCA Sustainability

ratings

ratings - Significantly lower MCA Shadow Carbon Cost impact

- More upside to MCA Valuation

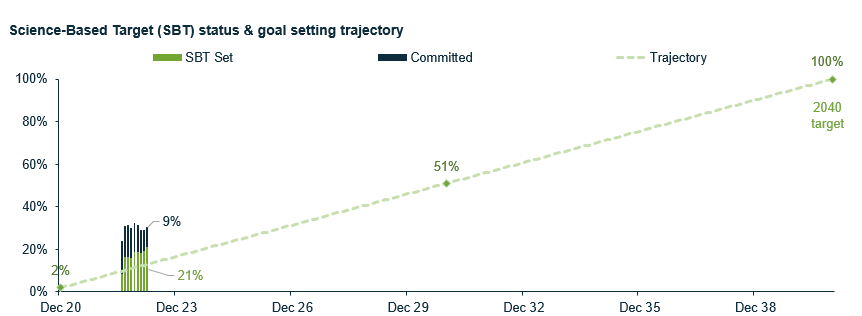

Martin Currie became a signatory to the Net Zero Asset Managers Initiative (NZAMI) in July 2021. We have committed our Sustainable Equity portfolios to be managed in-line with the goal of ‘Net Zero’ greenhouse gas emissions by 2050’. By 2040, we have aimed for 100% of portfolio holdings to have a Science-Based Target (SBT) to order to achieve this. Based on our current portfolio, 21% of portfolio holdings have an SBT, while a further 9% have publicly committed to setting an SBT. We are excited that this is ahead of target based on a linear trajectory.3

An active pathway to a Sustainable future

-

Click here to find out more about the Martin Currie Australia Sustainable Equity strategy.

Click to display all sources >>

1Past performance is not guide to future returns. The investment vehicles shown may have different risk profiles and a direct comparison may not be appropriate.

Source: Martin Currie; as of 31 May 2023. Martin Currie Australia (MCA) claims compliance with the Global Investment Performance Standards (GIPS®). The Sustainable Equity (EQ_19) composite contains fully discretionary Australian Equity accounts containing diversified portfolios of Australian Equity securities that have long-term sustainability in their business models. For comparison purposes the composite is measured against the S&P/ASX 200 Accumulation Index. For purposes of compliance with the GIPS®, the Firm is defined as Martin Currie Australia (“MCA”) formerly Legg Mason Australian Equities (LMAE), and comprises all assets managed or advised on a discretionary or non-discretionary basis. MCA is a division of Franklin Templeton Australia Limited (FTAL), which is a part of Franklin Resources, Inc. MCAs predecessor firm for GIPS® purposes, was FTAL, which was known as Legg Mason Asset Management Australia Limited (LMAMAL) prior to 1 October 2021. The MCA team has and continues to manage the Australian domestic equities portfolio of FTAL. The Australian Dollar is the currency used to express performance. Returns are presented gross of investment management fees, custody fees, administration fees, tax and net of trading expenses, and include the reinvestment of distribution income. Returns are presented net of non-reclaimable withholding taxes. GIPS Reports and/or the firm’s list of and description of composites and limited distribution pooled funds and list of broad distribution pooled funds can be obtained by contacting MCAClientService@martincurrie.com.au. Inception date: 1 June 2020.

GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

2 Past performance is not a guide to future returns.

Source: Martin Currie Australia; MSCI, Ownership Matters; as of 31 March 2023.Data calculated for the representative Martin Currie Australia Sustainable Equity portfolio. Index: S&P/ASX 200 Accumulation.

3Source: Martin Currie Australia, Macquarie Research; as of 31 March 2023. Data calculated for the representative Martin Currie Australia Sustainable Equity portfolio. Trajectory is based on a 2% baseline as of the end of 2020. More information about our firm's commitment can be found here: https://www.netzeroassetmanagers.org/signatories/martin-currie-investment-management/

Important information

This information is issued and approved by Martin Currie Investment Management Limited (‘MCIM’), authorised and regulated by the Financial Conduct Authority. It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. Martin Currie has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The views expressed are opinions of the portfolio managers as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee of future results or investment advice.

Some of the information provided in this document has been compiled using data from a representative account. This account has been chosen on the basis it is an existing account managed by Martin Currie, within the strategy referred to in this document. Representative accounts for each strategy have been chosen on the basis that they are the longest running account for the strategy. This data has been provided as an illustration only, the figures should not be relied upon as an indication of future performance. The data provided for this account may be different to other accounts following the same strategy. The information should not be considered as comprehensive and additional information and disclosure should be sought.

The information provided should not be considered a recommendation to purchase or sell any particular strategy / fund / security. It should not be assumed that any of the securities discussed here were or will prove to be profitable.

It is not known whether the stocks mentioned will feature in any future portfolios managed by Martin Currie. Any stock examples will represent a small part of a portfolio and are used purely to demonstrate our investment style.

The analysis of Environmental, Social and Governance (ESG) factors forms an important part of the investment process and helps inform investment decisions. The strategy/ies do not necessarily target particular sustainability outcomes.

Risk warnings – Investors should also be aware of the following risk factors which may be applicable to the strategy shown in this document.

- Investing in foreign markets introduces a risk where adverse movements in currency exchange rates could result in a decrease in the value of your investment.

- This strategy may hold a limited number of investments. If one of these investments falls in value this can have a greater impact on the strategy’s value than if it held a larger number of investments.

- Smaller companies may be riskier and their shares may be less liquid than larger companies, meaning that their share price may be more volatile.

- The strategy may invest in derivatives (index futures) to obtain, increase or reduce exposure to underlying assets. The use of derivatives may restrict potential gains and may result in greater fluctuations of returns for the portfolio. Certain types of derivatives may become difficult to purchase or sell in such market conditions.