Content navigation

The changing shape of China

In this instalment of our Evolving Landscape series, we discuss the disconnect between share prices and fundamentals, creating a significant investment opportunity.

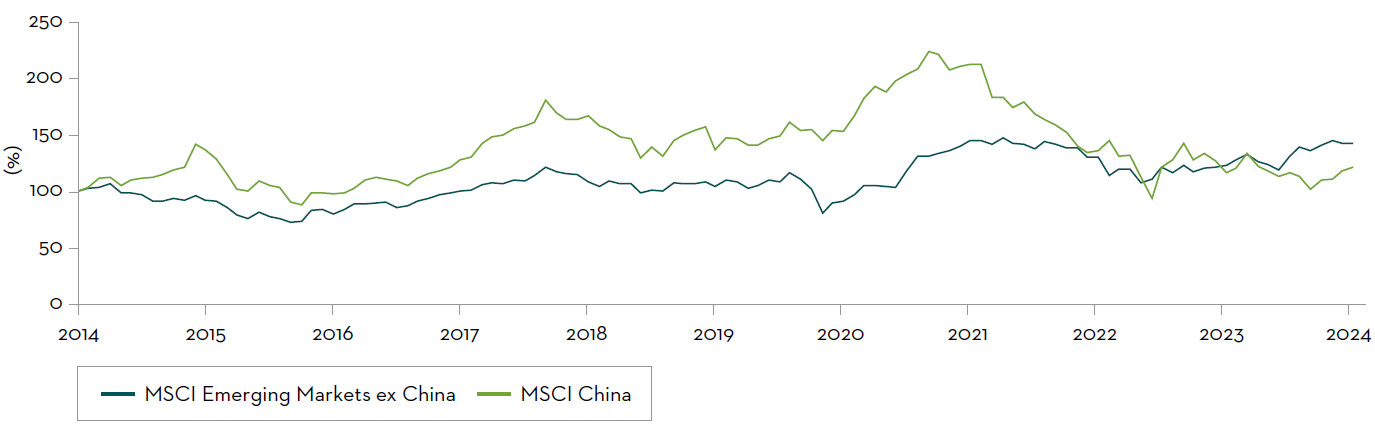

In 2023, the MSCI China index was down 11%, while MSCI Emerging Markets (EM) ex. China Index was up 20% – a performance gap of over 30%. From the end of 2018 to the end of 2023, this performance gap had increased to over 50%.1

This recent underperformance of China versus other EM countries has dragged down asset class returns, causing some investors to question their overall allocation to it. There are three primary concerns relating to the performance of Chinese equity markets:

- The domestic economy and the real estate market in particular

- Geopolitics (especially China-US relations)

- Finally, the direction of domestic policy as it relates to the private sector

These concerns have led to a material valuation derating in equity markets – a persistent selloff evidenced by the MSCI China Index performance below.

Performance of MSCI China Index and MSCI Emerging ex China Index over the past 10 years

Source: FactSet, as of 30 June 2024.

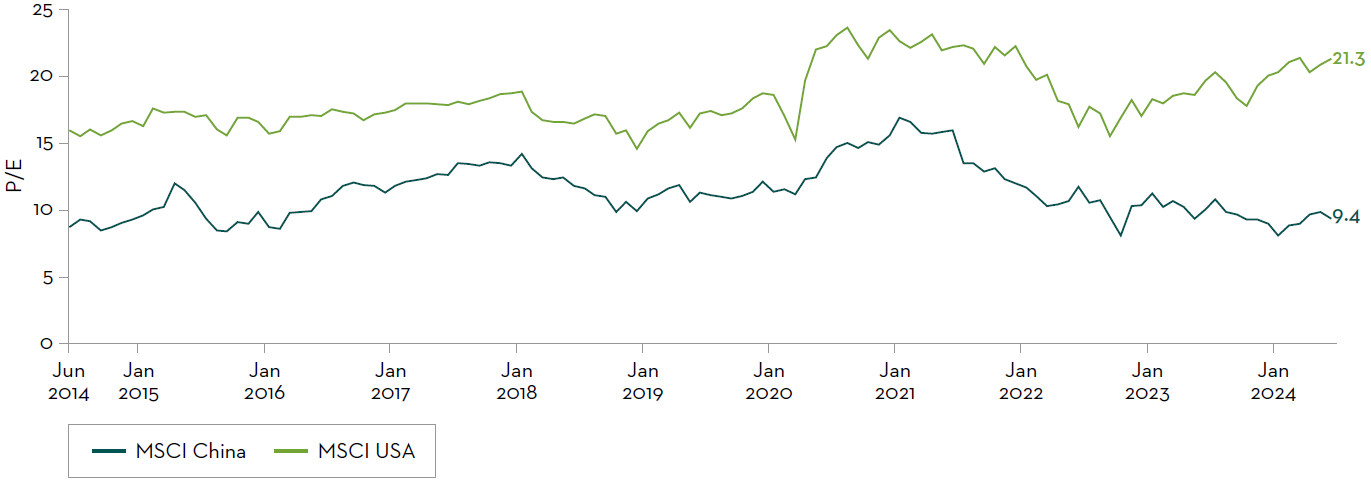

But we think China presents a counter consensus valuation opportunity. An analysis of the Price/Earnings (P/E) multiple yields interesting results, especially in the context of the strength which we have seen in US markets and can be illustrated in the chart below. China is trading on 9.4x – less than half of the multiple of the US at 21.3x. Put into the context of a ten-year history, we see that, compared to the US market, China has more valuation upside to its average and maximum P/E, with less downside to its minimum P/E.

P/E Multiples of MSCI China and MSCI USA over the past ten years

Source: FactSet, as of 30 June 2024.

-

But we think China presents a counter consensus valuation opportunity.

Chinese companies are delivering on fundamentals

At Martin Currie, we use bottom-up, fundamental analysis to identify what we believe to be the best opportunities in EM equities. By examining all our Chinese equity holdings, it is clear that despite the broader valuation derating in the Chinese market, there are many companies which continue to deliver operationally. The table below shows this at a stock level – the projected earnings growth for 2024 for each stock, alongside current P/E in the context of its five-year average (range and mean). For all our strategy’s Chinese holdings, the P/E sits within the range seen in the past five years and every stock is near or at its five year low.

Strategy portfolio holdings P/E and earnings

Source: Bloomberg and FactSet, 31 May 2024. *Meituan shows the P/B multiple instead of P/E due to data availability.

We have already begun to see some green shoots in 2024 as the market began to reward operational delivery in the Chinese market. During the first quarter results season, companies meeting or beating consensus estimates saw a positive market response, which is not something we saw consistently across 2023 when companies derated regardless of the nature of their results. Although this has not been consistent in 2024 so far, we are optimistic that this is the start of a more rational period in which markets return to fundamentals rather than sentiment alone.

Government intervention will support the real estate market

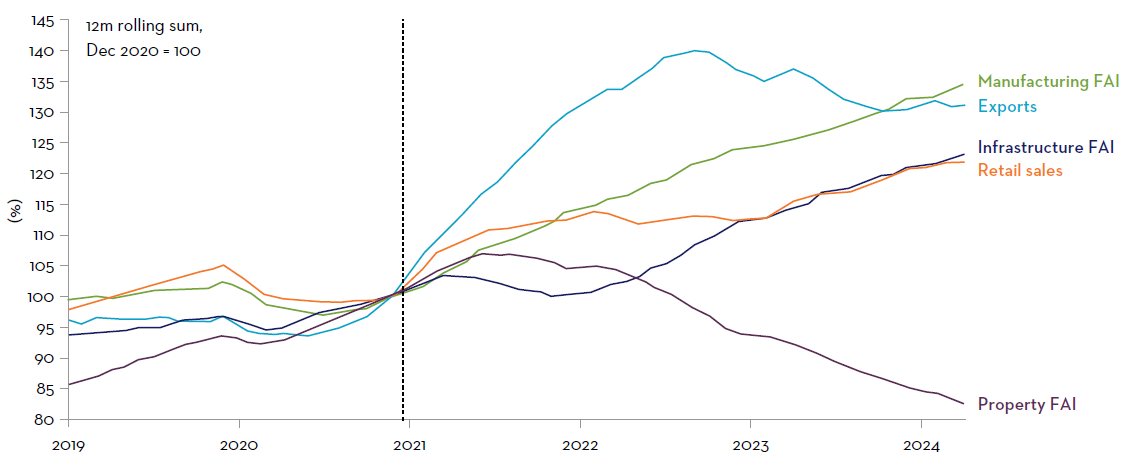

The recent weakness in the Chinese real estate market has become apparent due to years of unsustainable growth. This has had a domino effect in terms of sentiment across all other industries. However, as evidenced below, the main sectors of the Chinese economy outside of real estate have actually grown between 2018 – 2024 as illustrated by the chart below, despite the shorter-term weakness during the 2020 pandemic.

Performance of key segments of the Chinese economy

Source: Macquarie as of 31 May 2024. China Customs, WIND, Macquarie Macro Strategy. December 2020=100, 12 months rolling sum.

FAI = Fixed Asset Indicator, an economic indicator.

The worry is that the real estate sector is going to cause the broader Chinese economy to spiral out of control because it is such a key part of the Chinese market, an influencing factor in the market’s derating.

But we think this is unrealistic.

We believe that the government will act to stabilise the real estate market, a key step which should also improve consumer confidence. In doing so, it will unlock a positive virtuous cycle on the Chinese economy. This is the single biggest thing that the Chinese government can do. We have already seen a steady flow of policy support and we expect it to intensify, given that a lot of the excess has already been taken out of the real estate sector.

US-China relations are improving

We believe we are heading towards a more stable relationship between the US and China – a sufficiently positive step for the market. A crucial example of this improvement was in November 2023 when Chinese president Xi Jinping stated that the “earth is big enough for both our countries to succeed” following a meeting with President Joe Biden.2 This positive signal is not unique and we expect that it signals a calmer period of geopolitics, which should be supportive of equity markets.

Domestic policy increasingly supportive of private sector

China’s policymakers are increasingly signalling that private firms are needed in China and economic growth remains a priority. China knows that private firms are needed to achieve their economic desires. The electric vehicle battery sector is an example where the government has provided subsidies, tax breaks and buyer incentives to promote investment, growth and export success of private sector companies. This has helped China become a world-leading producer and consumer of both EV batteries and battery-powered cars.3

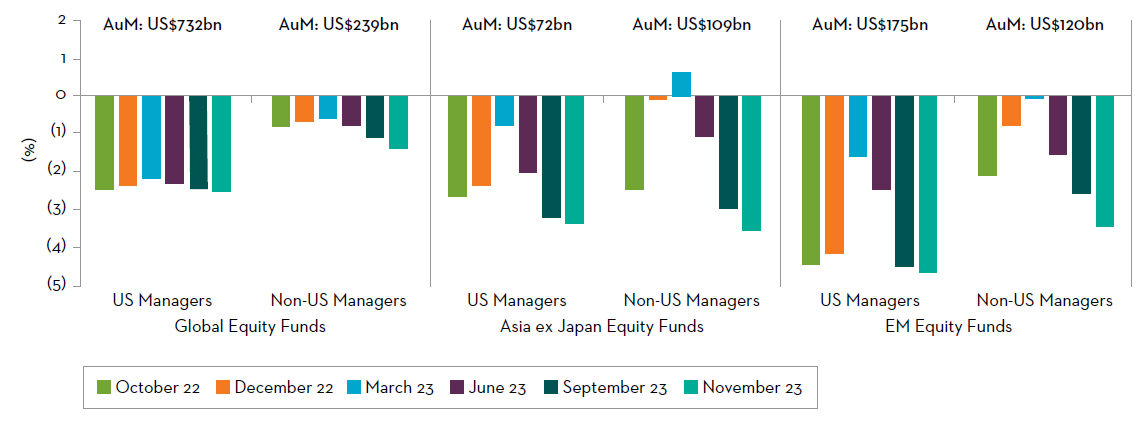

While the private sector is poised for government-encouraged growth, investors are very negatively positioned. A structural underweight to Chinese equities is one of the most consensus trades in global equities, as shown below. Across all main allocator buckets, investors are on average three to four percent underweight China. Simply moving towards a neutral position in China would represent billions of dollars of inflows into Chinese equities. This creates significant upside potential.

Position of active long-only managers in China/Hong Kong

Source: Morgan Stanley as at 5 December 2023. Position of Active Long-Only Managers in China/HK.

Positive sentiment

Despite the challenges presented by the Chinese market, there are several indicators that suggest a positive outlook for investors. The government’s anticipated stabilisation of the real estate market, the decrease in geopolitical tensions with the US, and the return of an equity market driven by fundamentals rather than flows, all of which should help to reduce uncertainty and raise confidence in China. This may then encourage global allocators to shift towards a more neutral or even overweight position in China. In our opinion, these factors will increase positive sentiment towards China and, by extension, the EM asset class.

Sources

1Source: FactSet, as at 31 May 2024.

2Sky News as at 16 November 2023, https://news.sky.com/story/biden-xi-talks-chinas-president-says-earth-is-big-enough-for-both-our-countries-to-succeed-13009244

3Statista and EV-Volumes, May 2023. Reuters, https://www.reuters.com/business/autos-transportation/china-announces-extension-purchase-tax-break-nevs-until-2027-2023-06-21/

Important Information

This information is issued and approved by Martin Currie Investment Management Limited (‘MCIM’), authorised and regulated by the Financial Conduct Authority. It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. Martin Currie has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.

This document may not be distributed to third parties. It is confidential and intended only for the recipient. The recipient may not photocopy, transmit or otherwise share this [document], or any part of it, with any other person without the express written permission of Martin Currie Investment Management Limited.

This document is intended only for a wholesale, institutional or otherwise professional audience. Martin Currie Investment Management Limited does not intend for this document to be

issued to any other audience and it should not be made available to any person who does not meet this criteria. Martin Currie accepts no responsibility for dissemination of this document to a person who does not fit this criteria.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The distribution of specific products is restricted in certain jurisdictions, investors should be aware of these restrictions before requesting further specific information.

The views expressed are opinions of the portfolio managers as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee

of future results or investment advice. There can be no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realised.

Some of the information provided in this document has been compiled using data from a representative account. This account has been chosen on the basis it is an existing account managed by Martin Currie, within the strategy referred to in this document.

Representative accounts for each strategy have been chosen on the basis that they are the longest running account for the strategy. This data has been provided as an illustration only, the figures should not be relied upon as an indication of future

performance. The data provided for this account may be different to other accounts following the same strategy. The information should not be considered as comprehensive and additional information and disclosure should be sought.

The information provided should not be considered a recommendation to purchase or sell any particular strategy/ fund/security. It should not be assumed that any of the securities discussed here were or will prove to be profitable.

It is not known whether the stocks mentioned will feature in any future portfolios managed by Martin Currie. Any stock examples will represent a small part of a portfolio and are used purely to demonstrate our investment style. Holdings are subject to change.

Risk warnings – Investors should also be aware of the following risk factors which may be applicable to the strategy shown in this document.

All investments involve risk including the potential for loss.

- Investing in foreign markets introduces a risk where adverse movements in currency exchange rates could result in a decrease in the value of your investment.

- This strategy may hold a limited number of investments. If one of these investments falls in value this can have a greater impact on the strategy’s value than if it held a larger number of investments.

- Smaller companies may be riskier and their shares may be less liquid than larger companies, meaning that their share price may be more volatile.

- Emerging markets or less developed countries may face more political, economic or structural challenges than developed countries. Accordingly, investment in emerging markets is generally characterised by higher levels of risk than investment in fully developed markets.

- The strategy may invest in derivatives Index futures and FX forwards to obtain, increase or reduce exposure to underlying assets. The use of derivatives may result in greater fluctuations of returns due to the value of the derivative not moving in line with the underlying asset. Certain types of derivatives can be difficult to purchase or sell in certain market conditions.

For wholesale investors in Australia:

This material is provided on the basis that you are a wholesale client. MCIM has entered an Intermediary arrangement with Franklin Templeton Australia Limited (ABN 76 004 835 849) (AFSL No. 240827) (FTAL) to facilitate the provision of financial services by MCIM to wholesale investors in Australia. Franklin Templeton Australia Limited is part of Franklin Resources, Inc., and holds an Australian Financial Services Licence (AFSL No. AFSL240827) issued pursuant to the Corporations Act 2001.

For professional investors in Canada.

This material is intended for residents in, or incorporated in, Canada and are a Permitted Client for the purposes of MI 31-103. The information on this section of the website is not intended for use by any other person, including members of the public.

Martin Currie Inc, incorporated in New York with its registered office at 280 Park Avenue, New York, NY 10017 and having a UK branch registered in Scotland (no SF000300), Head office, 5 Morrison Street, 2nd floor, Edinburgh, EH3 8BH, Tel: +44 (0) 131 229 5252 Fax: +44 (0) 131 222 2532 www.martincurrie.com, operates under the International Adviser Exemption with the Ontario Securities Commission (‘OSC’) and is therefore currently not required to be registered as a portfolio manager for the purposes of MI 31-103. Martin Currie Inc. is also authorised by the UK Financial Conduct Authority.

For the avoidance of doubt, nothing excludes, limits or restricts our obligations to you under the UK Financial Services and Market Act 2000, National Instruments or any other applicable law or regulation.

The opinions and views in this website do not take into account your individual circumstances, objectives, or needs and are not intended to be recommendations of particular financial instruments or strategies to you.

This website does not identify all the risks (direct or indirect) or other considerations which might be material to you when entering any financial transaction. You should consult with your professional advisers before undertaking any investment activity. The information provided on this website should not be treated as advice or a recommendation to buy or sell any particular security or other investment. The information on this website has not been reviewed by any competent regulatory authority.

For professional investors:

In the People’s Republic of China:

This document does not constitute a public offer of the strategy, whether by sale or subscription, in the People’s Republic of China (the “PRC”). These strategies are not being offered or sold directly or indirectly in the PRC to or for the benefit of, legal or natural persons of the PRC.

Further, no legal or natural persons of the PRC may directly or indirectly purchase any of the strategy or any beneficial interest therein without obtaining all prior PRC’s governmental approvals that are required, whether statutorily or otherwise. Persons who come into possession of this document are required by the issuer and its representatives to observe these restrictions.

In Hong Kong:

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

In South Korea:

This document is for information purposes only. It is prepared and presented to provide an introduction to the business of MCIM and its related companies (collectively known as ‘Martin Currie’). This document does not constitute an offer to sell or a solicitation of any offer to invest in any security, fund or other vehicle managed or advised by Martin Currie.

None of the security(ies), fund(s) or vehicle(s) managed by or advised by Martin Currie are registered in South Korea under the Financial Investment Services and Capital Markets Act of Korea and accordingly, none of these instruments nor any interest therein may be offered, sold or delivered, or offered or sold to any person for re-offering or resale, directly or indirectly, in South Korea or to any resident of South Korea except pursuant to applicable laws and regulations of South Korea.

Martin Currie is not registered with or regulated by any regulatory authorities in South Korea.

Copyright © 2024 Franklin Templeton. All rights reserved. Investment Products: NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE