Content navigation

Key takeaways:

- UK equity relative valuations are near their all-time lows.

- We believe the market is discounting an excess of bad news based on cyclical forces that are set to pass.

- When negative sentiment peaks, the opportunity for attractive future returns is arguably at its greatest.

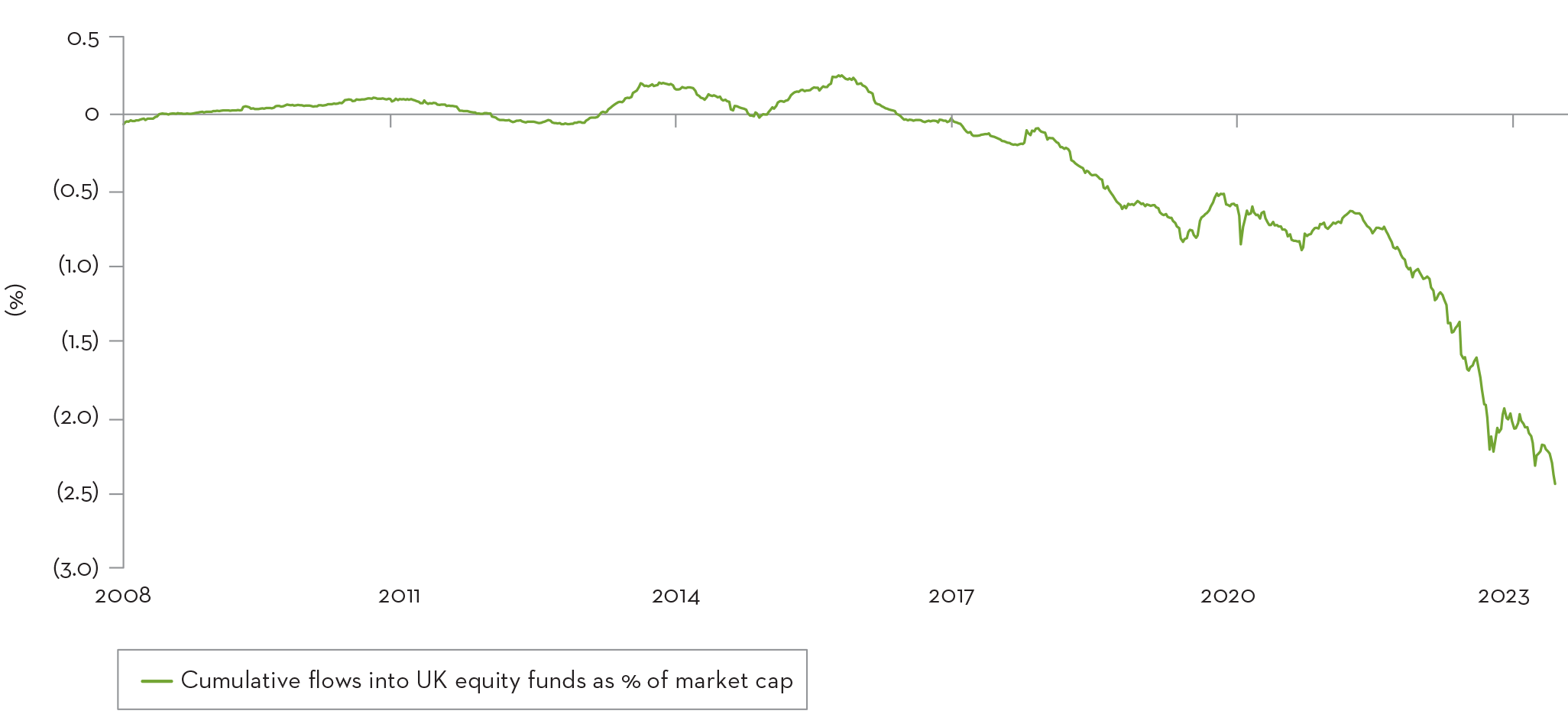

Times have been tough for the UK since 2016 when pollers marginally voted to leave the European Union. Investors fearful of hampered international trade and sluggish growth shunned the region en masse, and strategic asset allocations followed suit (figure 1).

But today the economy demonstrates many unique characteristics which, after a period of strong relative returns for the FTSE, may lead institutional investors to reconsider their tactical and strategic UK equity allocations, and could attract capital flows into the region.

Figure 1: Cumulative flows into UK Equity funds

Source: Credit Suisse, 28th June 2023.

-

With tax thresholds remaining flat for many years now, an increase in real wages provides greater income to the government as employees breach new tax brackets, thus delivering a marginal improvement to national finances.

Inflation proving stickier than hoped

We must be aware of the inflation story within the UK where core inflation is defying global trends, exceeding both the Eurozone and the US.

A significant contributor to this pain is the degree of private sector wage growth within the UK, which after a period of moderation is now starting to accelerate and is up at 8.2%.

In real terms however, wage growth does remain negative although this is expected to turn positive later this year should inflation abate as expected (figure 2).

Green shoots may be appearing – the latest UK core inflation print came in below analysts expectations which delivered an instant bounce in the UK equity market, but core goods still increased 6.9% year-on-year which remains eyewatering relative to other developed regions.

With economists estimating that wage growth of around 3% is necessary to curb inflation, a moderate overshooting from central bankers can be expected and base rate expectations are now settling at somewhere around 6%.

We must remain mindful of the impact that wage growth has on government finances. With tax thresholds remaining flat for many years now, an increase in real wages provides greater income to the government as employees breach new tax brackets, thus delivering a marginal improvement to national finances (holding all else constant).

Figure 2: UK real wage growth

Source: Credit Suisse, 28th June 2023.

But retailers holding up well

Figure 3: UK retail sales and consumer confidence

Source: Company data, Credit Suisse estimates.

At first this interest rate trajectory would seem disastrous for already squeezed consumer budgets, but we believe that retailers will reap reward in the months ahead as consumer confidence continues to demonstrate resilience (figure 3).

Grocery price inflation looks to have peaked as shoppers change their purchasing habits, real wage growth should turn positive by the end of this year which partly offsets the impact of rising debt costs, excess savings remain close to all time highs very high relative to history despite some depletion since 2020, and online sales as a percentage of total sales are back to their pre-pandemic trend – all supportive of the retailers which constitute a large proportion of the FTSE 350 index.

-

With banks reluctant to tighten credit conditions and the UK consumer still retaining excess savings of over 10% of GDP, a healthy buffer exists to defend against any extended turbulence.

What about rising interest rates?

Rising interest rates impact the UK consumer in many different ways – credit cards, loans, and mortgages to name just three. But the degree of interest rate sensitivity is not universal across the economy. In fact, at present the UK is less rate-sensitive than it has been in the past. Only 28% of UK homes are financed with a mortgage, compared to near 40% in the 1980s. Only 18% of mortgages are financed on a variable rate and just 50% of mortgages would have repriced by the end of 2023.

Figure 4: Average annual mortgage payment rises assuming mortagage rates run at 6%

Source: HSBC, 25th June 2023.

Indeed, the majority of UK mortgages are financed on 5-year fixed rates. The message here is that an interest rate shock takes its time to feed through to the UK consumer (figure 4), and the structural characteristics of the UK housing market (limited supply, rising rents, strong wage growth) provides some protection against an immediate collapse in real property prices.

With banks reluctant to tighten credit conditions and the UK consumer still retaining excess savings of over 10% of GDP, a healthy buffer exists to defend against any extended turbulence.

The government is not immune to the rising cost of debt either – the average term of government debt is around 5 years – therefore refinancing costs have multiplied. The short-term offset for the government is that sticky inflation increases VAT income, but the lagged effect of interest rate rises remains prominent and will drip through over time upon debt maturity.

Skilled immigration supporting long term demand

Inward net-migration to the UK rose to an all-time calendar year high of 606,000 last year (figure 5). But the nature of immigration has shifted significantly from unskilled EU labour in favour of skilled, non-EU labour in recent years.

This coincided with a historically tight labour market in 2022 but a disproportionate degree of vacancies exist in low-skilled jobs which were historically undertaken by EU workers.

With skilled, non EU workers ineligible to take many of these positions due to visa conditions, it is no surprise to see these sectors contributing more to growing wage pressures thus inflation.

Whilst the net skilled immigration is not totally offsetting this impact, there is a structural trend at play here. Over the long term, skilled immigration increases the demand for the UK’s homes, goods, and services.

Figure 5: Net migration to UK (4-quarter rolling total)

Source: HSBC, 30th May 2023.

Clearly this does not help the short term inflationary woes, but the contributions of migrants to the health service and various other sectors that they may work in, in addition to the tax paid on income and expenditure, supports the case for structural demand within the shores of the UK over the long term.

What does this mean for UK plc?

Some facts may help set the scene – inflation is expected to be a problem in the UK (at least in the short term), government finances will improve at the margin as a result (all else held constant), consumers are confident, but the impact of rising interest rates will take some time to feed through to the economy, and the UK has been subject to an insurge of skilled immigration. Clearly there are opposing forces at play here but our view is that the perceived ‘negatives’ for the economy are cyclical/transient factors that can be managed.

Tackling the inflation problem, interest rates will likely remain modestly higher for longer and the economy will adapt to a ‘new normal’ base case, supported by consumer confidence and excess savings. We must remain mindful that a stronger economy often means higher rates.

On the other hand, the ‘positives’ are secular – improved national finances and structural demographic shifts may enhance long term demand within the region for domestic and international investors alike. The recently announced Mansion House package is set to reform financial markets through renewed investment in UK plc, aiming to attract £50bn into high growth UK assets by 2030 and re-assert the LSE as a primary listing venue for rapidly growing corporations.

Although a nascent concept, the tailwinds that this could present are significant with aspirations to transform the UK into a research-intensive innovation hub, a far cry from the ‘old economy’ perception that the market has earned in recent years.

UK equity relative valuations are near their all-time lows. We are of the view that the market is discounting an excess of bad news based on cyclical forces that are set to pass, potentially overlooking the region’s long term attractiveness. When myopy peaks, the opportunity for attractive future returns is arguably at its greatest.

Important Information

This information is issued and approved by Martin Currie Investment Management Limited (‘MCIM’). It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. Martin Currie has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.The distribution of specific products is restricted in certain jurisdictions, investors should be aware of these restrictions before requesting further specific information.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The distribution of specific products is restricted in certain jurisdictions, investors should be aware of these restrictions before requesting further specific information.

The views expressed are opinions of the named manager as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee of future results or investment advice.

The analysis of Environmental, Social and Governance (ESG) factors forms an important part of the investment process and helps inform investment decisions. The strategy/ies do not necessarily target particular sustainability outcomes.

Risk warnings - Investors should also be aware of the following risk factors which may be applicable to the strategy shown in this document.

- Investing in foreign markets introduces a risk where adverse movements in currency exchange rates could result in a decrease in the value of your investment.

- This strategy may hold a limited number of investments. If one of these investments falls in value this can have a greater impact on the strategy’s value than if it held a larger number of investments.

- Smaller companies may be riskier and their shares may be less liquid than larger companies, meaning that their share price may be more volatile.’

- Income strategy charges are deducted from capital. Because of this, the level of income may be higher but the growth potential of the capital value of the investment may be reduced.