Content navigation

Will there be a clean sweep by either the Democrats or the Republican parties, and will there be lengthy recounts? These are two questions to focus on when looking at the financial market implications from a win by either Kamala Harris or Donald Trump.

With the US presidential elections fast approaching, we assess the potential impact on markets based on the two candidates proposed economic and international policies.

We conclude that a Trump presidency could lead to a more inflationary environment, but one potentially more supportive to corporate profits and earnings growth from lower taxes. Blanket tariffs, with a particular focus on China, could contribute to inflation and a more hawkish US Federal Reserve (Fed). With a stronger US dollar (USD), and with less certainty around his international policies, this increases the risk for international and emerging markets (EM) equities.

In contrast, a Harris presidency could have a negative impact on corporate profits from higher corporate tax rates, but this might be supportive of a benign inflationary environment. With a dovish Fed and a potentially weaker USD, this may be supportive for both EM equities, which tend to be supported by USD weakness, international equities, and the bond market. Less uncertainty on Harris’s international policies, given a likely continuation of Joe Biden’s, should result in less overall volatility across global financial markets.

Both candidates need to consider the impact of the expiry in 2025 of trillions of dollars of tax breaks from Donald Trump’s 2017 Tax Cuts and Jobs Act. If there are no cuts in fiscal expenditure, any benefits from the tax rises will be spent and the US budget deficit will remain at approximately 6% of Gross Domestic Product (GDP)1.

The key aspect to watch will be whether either candidate wins with a clean sweep, which would permit the winning candidate to apply more of their policy initiatives in a more meaningful manner. It all hangs on seven swing states, where polls are so narrow that the race is too close to call. There is also a risk of lengthy recounts, which could weigh on markets near term. Volatility in markets around the day of the results could open up a good opportunity for investors who focus on the longer-term picture, and who focus on fundamental dynamics for businesses and the economy.

-

Currently, the polls are very close, and neither candidate is shown to have a lead that is wide enough to be able to say that one candidate has a stronger probability of winning than the other.

Market and economy highlights

| Markets and Economy Implications | Harris | Trump | Comments |

|---|---|---|---|

| Corporate Taxes | Higher | Lower | Trump: Lowering the corporate tax rate to 18% a positive for corporates. But tariffs could weigh on margins if costs are not passed onto customers, which is negative for earnings growth. Harris: Proposing to increase corporate tax rates to 28% from 21%. |

| Corporate Profits | Lower | Higher | |

| Tariffs | Neutral | Higher | Trump: Blanket tariffs of 10-20% on all trading partners, and a minimum of 60% import tariffs on China proposed. This is likely inflationary, impacting consumer spending and real investment. Harris: Status quo maintained in trade policies. |

| Inflation | Neutral | Higher | Trump: Higher inflation risk from tariffs would likely push the Fed to a more hawkish stance. Resulting in higher interest rates and a strong USD. Harris: Higher tax revenues could help the budget deficit and support a benign/dovish monetary policy regime. This could be supportive for the economy and markets, but with a weaker USD. |

| Monetary Policies | Dovish | Hawkish | |

| US Dollar and Foreign Exchange (FX) | Weaker | Stronger | |

| Consumption | Neutral | Negative | Trump:The consumer would be less well off as a result of tariffs, the cost is passed onto the consumer eroding their purchasing power. Harris: No change of note. |

| Geopolitics | Positive | Negative | Trump: Greater uncertainty with lack of clarity on stance around various geopolitical hotspots. Tariffs could cause further tensions. Harris:Likely to continue the policies of the Biden administration, which means less uncertainty on the international scene. |

| Emerging Markets | Better | Worse | Trump: Less supportive backdrop with a stronger USD and the risk of tariffs, notably on China. Harris: More supportive with a weaker USD and more constructive international policy. |

| Market Volatility | Lower | Higher | Trump: Higher volatility with a less predictable approach to communication and a change in administration. Harris: Lower volatility with a perceived sense of continuity from previous administration. |

| Bond Markets | Higher |

Lower/ Neutral | Trump: Higher inflation and hawkish monetary policies could weigh on bond markets, but increased geopolitical risk could support government bonds. Harris: Lower inflation and a more dovish monetary policy should be supportive for bonds. |

Sector highlights

| Sectors | Harris | Trump | Comments |

|---|---|---|---|

| Consumer | Positive | Negative | Trump: Tariffs would risk increasing the Consumer Price

Index (CPI) reducing purchasing power. Harris: Positive on the margin for lower income consumers. |

| Industrials | Neutral | Neutral | Trump: Neutral but tariffs could increase the Producer

Power Index (PPI), but equally support some segments

from external competition. Harris: No change. |

| Energy | Negative | Positive | Trump: Supportive of traditional energy i.e. fossil fuels. Harris: Supportive of renewable energy. |

| Utilities | Mixed | Mixed | Trump: Increased support. Harris: Support for renewables is a negative for traditional utilities. |

| Financials | Positive | Negative | Trump: Less favourable yield curve due to inflation risk

would be less supportive for financials if the yield curve

flattens. Harris: A favourable yield curve would be more supportive to financials. |

| Healthcare | Negative | Neutral | Trump:Neutral on the sector. Harris: More pressure on drug pricing and medical costs are a negative for the sector. |

| Technology & Media | Negative | Positive | Trump:More friendly of Big Tech given a JD Vance

vice-presidency, but tariffs could significantly impact

the input costs in this sector. Harris: More focus on anti-monopolistic initiatives, which could weigh on Big Tech. |

| Telecoms | Neutral | Neutral | Trump: No policies of note. Harris: No policies of note. |

| Materials | Negative | Positive | Trump: Less focus on sustainability consideration is

positive. Harris: Negative given higher sustainability considerations. |

Overall, as always, the increased focus on the US presidential elections brings uncertainty in markets. One point of note is that it is never a given, in politics, that stated policies intentions will be implemented once a candidate is elected. There is also the added consideration of how Congress and the Senate are split - if there is a split between Democrats potentially winning back Congress, and the Republicans winning back the Senate, it will be difficult for any major policy initiatives to be voted through. This could end up being the lowest risk outcome for markets, at least in terms of volatility.

Notably, if Trump was to win the presidency, we understand that the blanket implementation of tariffs could not be implemented unilaterally by the presidency; it would need to be ratified by Congress, making it less likely that such policy will be applied if it is Democrat controlled. The scenario that carries the most potential for policy shifts is one where either one of the candidates’ parties takes control of both houses – a so-called clean sweep.

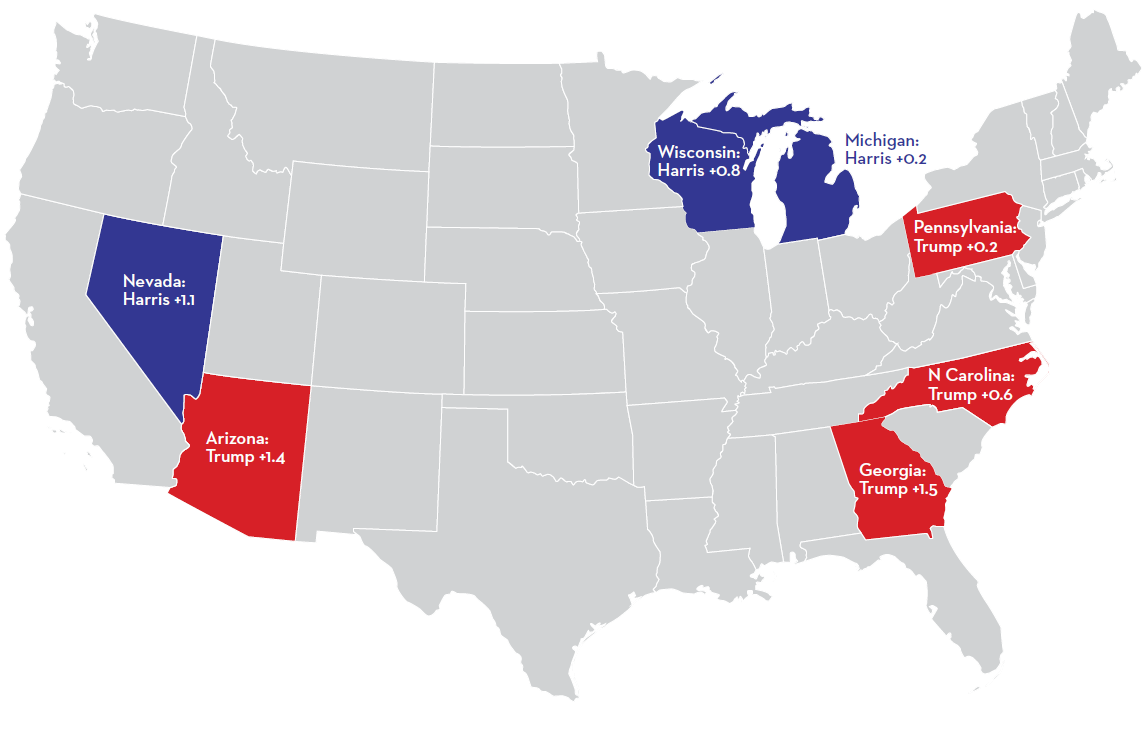

The importance of the seven swing states

Currently, the polls are very close, and neither candidate is shown to have a lead that is wide enough to be able to say that one candidate has a stronger probability of winning than the other. The importance of the swing states will be critical - there are seven swing states that will determine the outcome of the election. It appears that things will be very tight, and it is too close to call any outcome for certain.

As we write, polling averages point to Harris leading in Nevada, Michigan, and Wisconsin, whilst Trump is leading in Arizona, Georgia, and North Carolina, with Pennsylvania pointing to a tie. Polling margins in these states are however very narrow, which means that the race in these swing states is too close to call.

Average polls in the seven swing states

Source: Real Clear Politics as at 8 October 2024.

Short-term volatility but long-term opportunity

Given the closeness of the poll, there is a non-negligible risk of the elections going into close counts and recounts, which could delay the final outcome. Volatility in markets around the day of the results, notably if a final result is delayed, could open up a good opportunity for investors who focus on the longer-term picture, and the fundamental dynamics of businesses and the economy.

Sources

1Source: Federal Bank of St Louis as at 26 September 2024. Federal Surplus or Deficit [-] as Percent of Gross Domestic Product (FYFSGDA188S) | FRED | St. Louis Fed (stlouisfed.org)

Important Information

This information is issued and approved by Martin Currie Investment Management Limited (‘MCIM’), authorised and regulated by the Financial Conduct Authority. It does not constitute investment advice. Market and currency movements may cause the capital value of shares, and the income from them, to fall as well as rise and you may get back less than you invested.

The information contained in this document has been compiled with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. Martin Currie has procured any research or analysis contained in this document for its own use. It is provided to you only incidentally and any opinions expressed are subject to change without notice.

This document is intended only for a wholesale, institutional or otherwise professional audience. Martin Currie Investment Management Limited does not intend for this document to be issued to any other audience and it should not be made available to any person who does not meet this criteria. Martin Currie accepts no responsibility for dissemination of this document to a person who does not fit this criteria.

The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute, and may not be used for the purpose of, an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

Past performance is not a guide to future returns.

The distribution of specific products is restricted in certain jurisdictions, investors should be aware of these restrictions before requesting further specific information.

The views expressed are opinions of the portfolio managers as of the date of this document and are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. These opinions are not intended to be a forecast of future events, research, a guarantee of future results or investment advice.

Please note the information within this report has been produced internally using unaudited data and has not been independently verified. Whilst every effort has been made to ensure its accuracy, no guarantee can be given.

Some of the information provided in this document has been compiled using data from a representative account. This account has been chosen on the basis it is an existing account managed by Martin Currie, within the strategy referred to in this document.

Representative accounts for each strategy have been chosen on the basis that they are the longest running account for the strategy. This data has been provided as an illustration only, the figures should not be relied upon as an indication of future performance. The data provided for this account may be different to other accounts following the same strategy. The information should not be considered as comprehensive and additional information and disclosure should be sought.

The information provided should not be considered a recommendation to purchase or sell any particular strategy/fund/security. It should not be assumed that any of the securities discussed here were or will prove to be profitable.

It is not known whether the stocks mentioned will feature in any future portfolios managed by Martin Currie. Any stock examples will represent a small part of a portfolio and are used purely to demonstrate our investment style.

Risk warnings – Investors should also be aware of the following risk factors which may be applicable to the strategy shown in this document.

- Investing in foreign markets introduces a risk where adverse movements in currency exchange rates could result in a decrease in the value of your investment.

- This strategy may hold a limited number of investments. If one of these investments falls in value this can have a greater impact on the strategy’s value than if it held a larger number of investments.

- Smaller companies may be riskier and their shares may be less liquid than larger companies, meaning that their share price may be more volatile.

- Emerging markets or less developed countries may face more political, economic or structural challenges than developed countries. Accordingly, investment in emerging markets is generally characterised by higher levels of risk than investment in fully developed markets.

For wholesale investors in Australia:

This material is provided on the basis that you are a wholesale client. MCIM has entered an Intermediary arrangement with Franklin Templeton Australia Limited (ABN 76 004 835 849) (AFSL No. 240827) (FTAL) to facilitate the provision of financial services by MCIM to wholesale investors in Australia. Franklin Templeton Australia Limited is part of Franklin Resources, Inc., and holds an Australian Financial Services Licence (AFSL No. AFSL240827) issued pursuant to the Corporations Act 2001.

For professional investors in Canada.

This material is intended for residents in, or incorporated in, Canada and are a Permitted Client for the purposes of NI 31-103. The information on this section of the website is not intended for use by any other person, including members of the public.

Martin Currie Inc, incorporated in New York with its registered office at 280 Park Avenue, New York, NY 10017 and having a UK branch registered in Scotland (no SF000300), Head office, 5 Morrison Street, 2nd floor, Edinburgh, EH3 8BH, Tel: +44 (0) 131 229 5252 Fax: +44 (0) 131 222 2532 www.martincurrie.com , operates under the International Adviser Exemption with the Ontario Securities Commission (‘OSC’) and is therefore currently not required to be registered as a portfolio manager for the purposes of MI 31-103. Martin Currie Inc. is also authorised by the UK Financial Conduct Authority.

For the avoidance of doubt, nothing excludes, limits or restricts our obligations to you under the UK Financial Services and Market Act 2000, National Instruments or any other applicable law or regulation.

he opinions and views in this website do not take into account your individual circumstances, objectives, or needs and are not intended to be recommendations of particular financial instruments or strategies to you. This website does not identify all the risks (direct or indirect) or other considerations which might be material to you when entering any financial transaction.

You should consult with your professional advisers before undertaking any investment activity. The information provided on this website should not be treated as advice or a recommendation to buy or sell any particular security or other investment. The information on this website has not been reviewed by any competent regulatory authority.

For professional investors:

In the People’s Republic of China:

This document does not constitute a public offer of the strategy, whether by sale or subscription, in the People’s Republic of China (the “PRC”). These strategies are not being offered or sold directly or indirectly in the PRC to or for the benefit of, legal or natural persons of the PRC.

Further, no legal or natural persons of the PRC may directly or indirectly purchase any of the strategy or any beneficial interest therein without obtaining all prior PRC’s governmental approvals that are required, whether statutorily or otherwise. Persons who come into possession of this document are required by the issuer and its representatives to observe these restrictions.

In Hong Kong:

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

In South Korea:

This document is for information purposes only. It is prepared and presented to provide an introduction to the business of MCIM and its related companies (collectively known as ‘Martin Currie’). This document does not constitute an offer to sell or a solicitation of any offer to invest in any security, fund or other vehicle managed or advised by Martin Currie.

None of the security(ies), fund(s) or vehicle(s) managed by or advised by Martin Currie are registered in South Korea under the Financial Investment Services and Capital Markets Act of Korea and accordingly, none of these instruments nor any interest therein may be offered, sold or delivered, or offered or sold to any person for re-offering or resale, directly or indirectly, in South Korea or to any resident of South Korea except pursuant to applicable laws and regulations of South Korea.

Martin Currie is not registered with or regulated by any regulatory authorities in South Korea.